International payment methods

Different types of international payment methods

When it comes to trading of commercial goods, there is always a certain level of risk and trust involved. Whether you’re a buyer or seller, you are bound to be exposed to some risk when dealing with international transactions. In large part, the amount of risk involved highly depends on the method of payment you use.

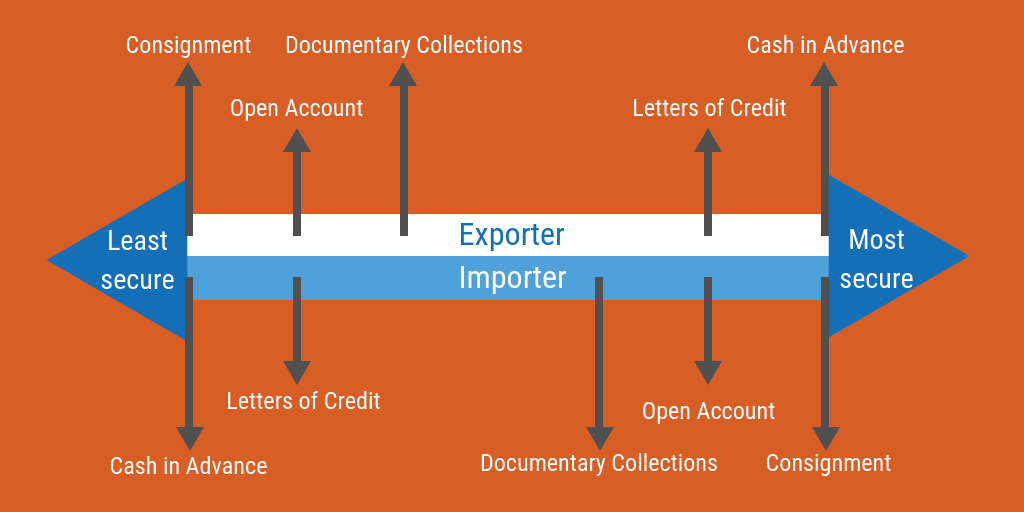

There are plenty of international paying methods for importers and exporters across the globe. And as the world continues to globalize, we’re seeing an increase in international payment modes. But as with Incoterms, the parties lying at the split ends of the spectrum have clashing agendas and priorities to fulfill and to look out for.

When it comes to cross-border payments, buyers tend to prioritize the cheapest and most straightforward payment method. In other words, anything that can help reduces cost. Another priority is ensuring they receive the goods specified.

While buyers prefer paying as late in the transaction process as possible, sellers will want to be paid in full, as quickly as possible, and via a secure option. Sellers who offer attractive payment terms and varying methods will have an advantage over those who limit themselves.

The main international payment methods used around the world today include:

In this article, we’ll discuss these commonly used international payment methods between importer and exporter as well as their pros and cons.

Cash in Advance

Also known as pre-payments, cash in advance is as it sounds. The buyer completes the payment and pays the seller in full before the merchandise is delivered and shipped off to the buyer.

While there are plenty of cash in advance payment methods available, credit card payment and wire transfers (electronic payment via banks) are the more commonly used payment modes.

While this is an attractive option for sellers, it’s presents a significantly high risk for buyers as it produces a disadvantageous cash flow and no definite guarantee of receiving the goods or the condition in which they arrive.

This is generally a recommended option for sellers who are dealing with new buyers or buyers with weak credit ratings, and/or for high-valued products.

Other cash in advance methods include:

- Debit card payment

- Telegraphic transfer

- International cheque

- etc.

Pros and Cons of Cash in Advance

| Party | Pros | Cons |

|---|---|---|

| Buyer | → Minimal | → Risk of not receiving shipment or receiving damaged shipment → Unfavorable cash flow |

| Seller | → Secure full payment before shipment No risk of non-payment → No risk of non-payment | → Risk of losing business to competitors if offering this as the only accepted international payment method |

Letters of Credit

A Letter of Credit is one of the most secure international payment methods for the importer and exporter as it involves the assistance of established financial institutions such as banks as an intermediary and a certain level of commitment from both parties.

With a Letter of Credit, payment is made through both the buyer and sellers’ banks. Upon confirmation of trade terms and conditions, the buyer instructs his bank to pay the agreed-upon sum by both parties to the seller’s bank. The buyer’s bank then sends a Letter of Credit as proof of sufficient and legit funds to the seller’s bank. Payment is only remitted after all stated conditions are met by both parties and shipment has been shipped.

Letters of Credit are also sometimes known as LC, bankers commercial credit or documentary credit.

Pros and Cons of Letters of Credit

| Party | Pros | Cons |

|---|---|---|

| Buyer | → Guarantee of cargo being shipped before payment → Obligation by seller to fulfill stated and negotiated conditions | → Reliance on seller to ship goods as specified |

| Seller | → Reliable proof of foreign buyers’ credit prior to shipment of goods → Obligation by buyer to fulfill stated and negotiated conditions → Payment by buyer’s bank in the event of a default → Low risk | → Minimal |

Documentary Collections

Documentary collections is a process in which both the buyer’s and seller’s banks act as facilitators of the trade.

The seller submits documents needed by the buyer, such as the Bill of Lading, which is necessary for the transfer of title to the goods, to its bank. The seller’s bank will then send these documents to the buyer’s bank along with payment instructions. The documents are only released in exchange for payment, which is remitted immediately or at a specified date in the future.

With documentary collections, also known as Bills of Exchange, the seller is basically handing over the responsibility of payment collection to his bank.

Pros and Cons of Documentary Collections

| Party | Pros | Cons |

|---|---|---|

| Buyer | → More economical than Letters of Credit | → More economical than Letters of Credit |

| Seller | → Minimal | → No verification involved → No guarantee of payment from bank → No protection against cancellations |

Open Account

Under Open Accounts (also known as Accounts Payable), merchandise are shipped and delivered prior to payment, proving to be an extremely attractive option for buyers especially in terms of cash flow. On the other end of the spectrum, however, sellers are faced with high risks.

With this payment option, the seller ships the goods to the buyers with a credit period attached. This is usually in 30-, 60-, or 90-day periods, during which the buyer must carry out full payment.

Open Accounts are usually only recommended for trustworthy and reputable buyers, for buyers and sellers who have an established and trusting relationship, and/or for exports with relatively lower value to minimize risk.

Pros and Cons of Open Account

| Party | Pros | Cons |

|---|---|---|

| Buyer | → Receives goods before payment is due → Positive cash flow | → Minimal |

| Seller | → Can attract customers in competitive markets | → High risk of default |

Consignment

The consignment process is similar to that of an open account whereby payment is only completed after the receipt of merchandise by the buyer.

The difference lies in the point of payment. With consignment, the foreign buyer is only obliged to fulfill payment after having sold the merchandise to the end consumer. This international payment method is based on an agreement under which the foreign seller retains ownership of the merchandise until it has been sold. In exchange, the buyer is responsible for the management and sale of the merchandise to the end customer.

Consignment is usually only recommended for buyers and sellers with a trusting relationship or reputable distributors and providers. Given the high risk involved, sellers should make sure they have adequate insurance coverage that can cover both the goods from transit to final sale and mitigate any damages caused in the event of non-payment by the buyer.

Pros and Cons of Consignment

| Party | Pros | Cons |

|---|---|---|

| Buyer | → Payment is due only after final sale of goods to end consumer → Quick receipt of goods | → May have large inventory to manage → Minimal |

| Seller | → Lower storage fees → Less inventory management → More competitive | → Payment not guaranteed until end sale → Lack of access to and management of merchandise |

- 1. Different types of international payment methods

- 2. Cash in AdvancePros and Cons of Cash in Advance

- 3. Letters of CreditPros and Cons of Letters of CreditDocumentary CollectionsPros and Cons of Documentary Collections

- 4. Open AccountPros and Cons of Open Account

- 5. ConsignmentPros and Cons of Consignment

Related Articles