IMO 2020 regulation and its impact on the shipping container trade

It is all the industry have been talking about these days. And a term you’ve seen floating around for years.

You don’t have to be an avid reader of ocean freight news to have heard of the term IMO 2020. But recognizing the term is one thing and knowing what it entails is another. Understanding how it affects your supply chain? That’s a whole other level.

The IMO 2020 is one of the most significant changes in the maritime sector in recent history and major cross-industry impacts. As we inch closer to its implementation date, it’s best to wrap your head around this new regulation.

In this article, we’ll dive into what the IMO 2020 is and its background, understand compliance methods, and how of all this affects you as a shipper.

What is IMO 2020?

The IMO 2020 is a regulation set by the International Maritime Organization that states that as of January 1, 2020, the sulfur emissions of all maritime vessels must be limited to 0.5% m/m (mass by mass), down from the current 3.5% m/m.

Here are snippets of IMO’s own explanation of the regulation broken down and explained.

“The main type of “bunker” oil for ships is heavy fuel oil, derived as a residue from crude oil distillation. Crude oil contains sulphur which, following combustion in the engine, ends up in ship emissions.”

“Bunker” oil is the type of fuel used by maritime shipping vessels. Also known as Heavy Fuel Oil (HFO), this type of fuel is obtained from crude oil through a refining process called distillation, which involves purifying the crude oil through heating and cooling to extract hydrocarbons such as gasoline and diesel.

The residual oil that is left after this process is known as bunker oil, which is used to power shipping vessels.

Crude oil itself contains sulfur elements that remain in the residual bunker oil even after distillation. These sulfur elements make up around 3.5% of its weight.

As shipping vessels burn and consume bunker oil, they emit sulfur into the atmosphere as a harmful byproduct.

“IMO regulations to reduce sulphur oxides (SOx) emissions from ships first came into force in 2005, under Annex VI of the International Convention for the Prevention of Pollution from Ships (known as the MARPOL Convention).

One of the main difficulties with regulating maritime pollution is the vast swaths of the ocean that are not governed by any state.

This is where the MARPOL Convention plays a role. Signed in 1973, it is an international agreement aimed at preventing maritime pollution by shipping vessels. As of today, over 155 countries have ratified the convention.

Various annexes have since been added to the original convention. The most relevant of which is Annex IV. Annex IV was added in 2005 and deals specifically with air pollution from maritime vessels.

Since then, the limits on sulphur oxides have been progressively tightened.

- 2005: Annex VI came into force and sulfur emissions limit was set at 4.5%

- 2008: Requirements of Annex VI was tightened

- 2010: Revised regulations came into force

- 2012: Sulfur emissions limit lowered from 4.5% to 3.5%

- 2013: Energy efficient requirements came into force

From 1 January 2020, the limit for sulphur in fuel oil used on board ships operating outside designated emission control areas will be reduced to 0.50% m/m (mass by mass).

The current sulfur limit of 3.5% m/m will be reduced to 0.5% starting 2020. This means that all fuel used by engines (both main and auxiliary) and boilers must be limited to a sulfur concentration of 0.5%.

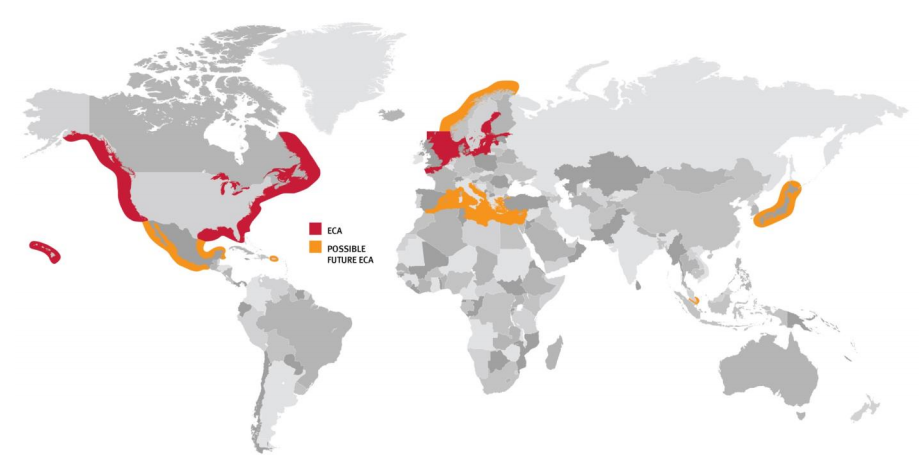

Emission Control Areas, also known as ECAs, are zones that have stricter rules and requirements on shipping emissions. The sulfur limit for ships in ECAs stands at 0.1% m/m.

Vessels operating in these areas must comply with the specific measures that have been set, usually pertaining to the reduction of nitrogen oxides and sulfur oxides emissions.

Current ECAs include the Baltic Sea, North Sea, several areas off the coasts of the US and Canada, and the US Caribbean Sea.

Image credit: DuPont

IMO 2020 compliance methods

Annually, more than 400 million tons of marine fuel is used to power shipping vessels. Of these, containerships with capacities of 4,000TEU and above make up a fifth of the total demand.

With heavy fuel oil no longer an option come 2020, shipowners must now look to alternative fuel methods.

Here are the three accepted methods for shipowners to comply with the IMO 2020 regulation.

Liquefied Natural Gas (LNG)

Deemed as one of the most environmentally attractive alternatives to heavy fuel oil, LNG can help reduce sulfur emissions by as much as 90%. It has been the fuel of choice for newly constructed vessels over the past five years.

The low sulfur content means LNG-powered vessels can operate in ECAs without having to change their fuel, as is the norm with oil-fueled vessels.

Demand for LNG

However, not all shipping vessels are equipped to carry LNG and the current infrastructure supporting the use of LNG remains limited in scope and availability.

Image credit: Shell

According to estimates, LNG-powered vessels will cost $5 million more to construct than oil-fueled vessels, a price that’s nearly equivalent to the cost of installing scrubbers.

Proponents of LNG have argued that LNG-powered vessels do not require as much maintenance as those powered by oil, which adds to their longevity.

Regardless, the option to switch to LNG does appear to be gaining steam; the industry has seen an increase in the number of orders for LNG-powered ships since 2015.

- No. of LNG-powered ships in 2015: 102

- No. of LNG-powered ships in 2017: 117

- No. of LNG-powered ships in 2019: 143 (and 135 more in the order books)

Scrubbers

Scrubbers refer to cleaning systems of exhaust gases. Vessels fitted with scrubbers can continue to carry and burn HFO.

Such systems work by cleaning emissions prior to its release into the atmosphere. This is done by introducing alkaline water into the exhaust, which reduces 98% of sulfur oxide elements.

Questions have, however, been raised over its sustainability and overall environmental benefits. Even though sulfur contents are reduced in the treatment process, the water used for the treatment is eventually released back into the sea.

Another challenge behind the use of scrubbers is that it isn’t being regulated by the IMO and must be approved by the vessels’ flag states. Certain countries, however, including Singapore and China, have banned the use of open loop scrubbers, the most widely used method.

That being said, one must consider the possibility that future environmental regulations may invalidate the use of scrubbers.

Demand for scrubbers

Energy consultancy firm Wood Mackenzie puts the number of orders for scrubbers at over 2,000. But that is just a fraction of the approximately 90,000 maritime vessels there are traversing the seas.

A likely reason for the scrubber-sceptic mindset may be due to the high costs of installation acting as a deterrence to shipowners. According to estimates, the cost of installing scrubbers stands at between $2 million and $6 million per vessel, depending on its age, type, and size.

Low Sulfur Fuel (LSF)

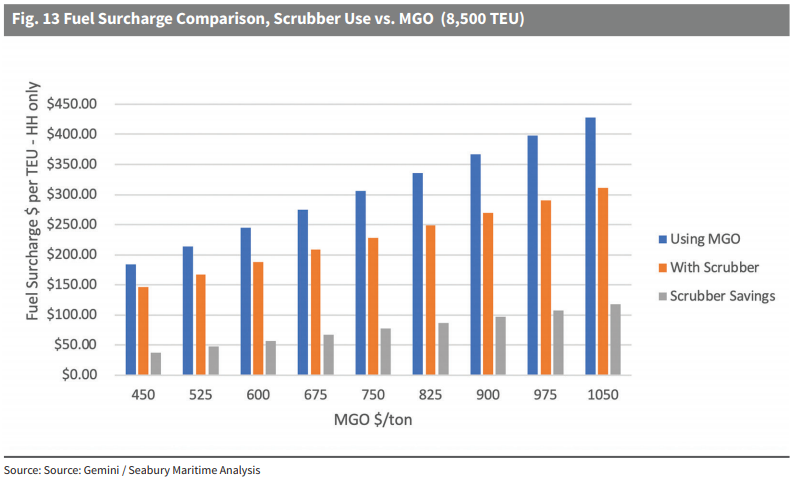

Low Sulfur Fuels such as Marine Gas Oil (MGO) is one of the highest quality marine fuels currently available on the market. It has a significantly lower sulfur concentration (of approximately 0.1%) but is also significantly more expensive than scrubbers.

As of February 2019, the per ton price for heavy fuel oil stood at $420, compared to $647 for MGO.

MGOs aside, major oil producers and refiners have already started working on creating new and cheaper types of low-sulfur mixtures to meet the new sulfur content requirements.

But even as progress is made, tests have so far suggested that these new blends are still not 100% stable and compatible. In addition, the low availability means it’s unlikely that many vessels will be equipped with new mixtures of low sulfur fuel during the initial period.

Demand for LSF

Of the options available, the switch to low sulfur fuel will likely be the most popular in the initial period, due to a lack of scrubber installations.

Industry experts say MGOs is the most hassle-free solution available and requires the fewest technical changes as vessels are already having to use this fuel type within ECAs.

Preparing for IMO 2020 as a shipper

Even though shipowners and liners are the ones having to comply with the new regulation, its effect is expected to be felt by shippers worldwide.

“As it stands, fuel costs make up more than half of the overall operating costs of a vessel. And with IMO 2020, this is expected to increase exponentially.”

- Aliona Yurlova, International Business Development expert at iContainers

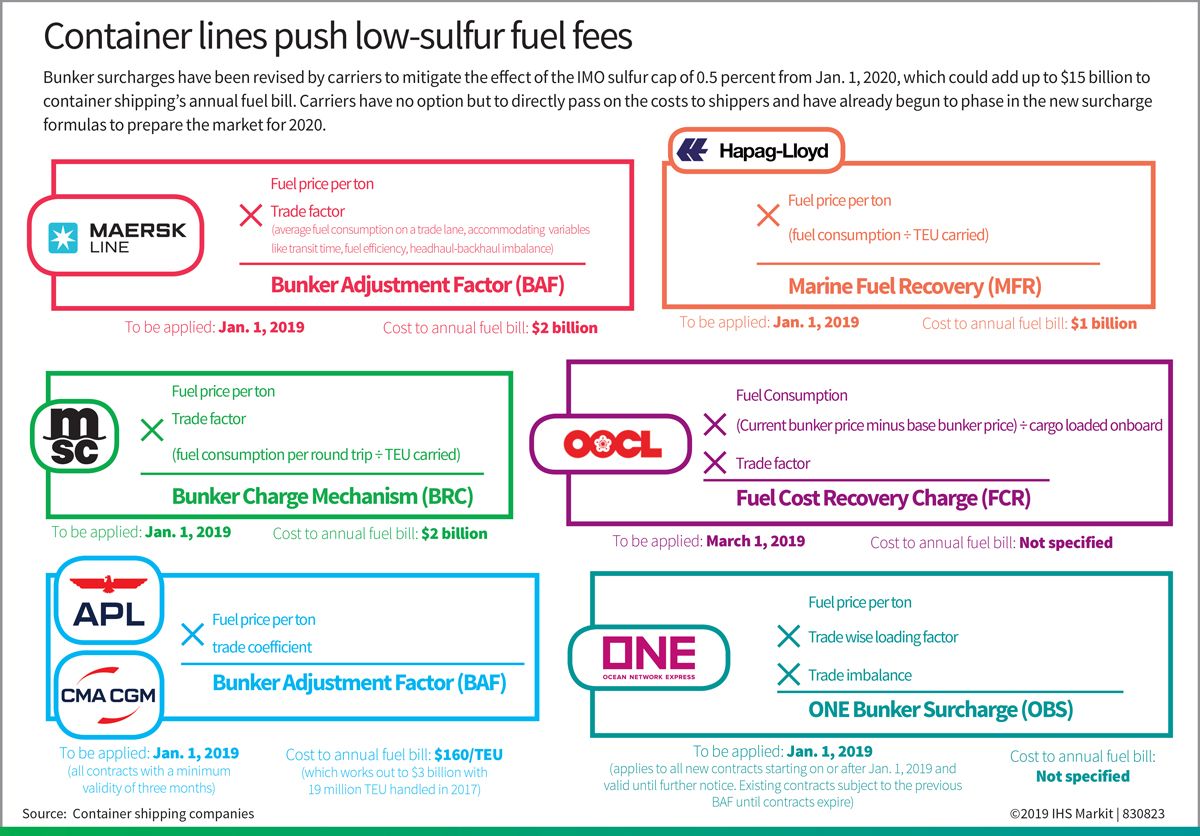

The total cost of compliance is expected to cost the shipping industry up to $15 billion annually, a part of which shipping carriers including CMA-CGM, ONE, OOCL, and APL have all said will be passed onto customers.

Image credit: IHS Markit

“One of its direct and long-term impacts will be on ocean freight rates and space availability. Shipping rates are expected to remain volatile, with at least two to three cost waves to hit shippers over the first year or two.

That said, there are ways that you, as a shipper, can better manage your shipments to avoid too much disruption to your supply chain.”

- Aliona Yurlova, International Business Development expert at iContainers

Monitor your trade lanes

Bunker surcharges will likely differ between trade lanes (eg. Pacific vs Atlantic). Analyze and assess your prevailing and annual trade lanes to pinpoint the best areas and moments where you can optimize costs.

When shipping during the peak season, plan in advance and consult your freight forwarder about seasonal General Rate Increases (GRI) and Peak Season Surcharges (PSS).

Rates negotiation

It’s important to understand the bunker surcharges being implemented by carriers, especially those who provide services for your desired shipment route.

Make sure you’re on top of all surcharges announcements (whether they will come into effect in January 2020, later, or sooner) and use any discrepancy between carriers as a negotiation tool.

Shipping large volumes grant will greater bargaining power for NAC or spot rates. Use that to your advantage. As a smaller player, consider streamlining other logistics services where possible to compensate for the increase in BAF.

Related Articles